Looking Past the Mag 7: Why Mid- and Small-Caps Could Outperform Going Forward

For a lot of investors, the idea of a broader risk rally outside of the ‘Magnificent Seven’ (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta Platforms and Tesla) requires clearing a few mental hurdles. After all, we’re not long removed from a pronounced late summer sell-off and the macro climate still feels temperamental with potential landmines still lurking. Nevertheless, given current valuations, those who choose to increase allocations to small and mid-caps at this point in the monetary policy cycle may expect to be rewarded relative to those that retain more broader exposures.

Below, we’ll go over the main reasons why investors should consider increasing satellite positions in small- and mid-cap stocks.

1) Macro backdrop isn’t as bad as you might think. For all the talk of an incoming ‘recession’ in the United States, forward-looking growth indicators don’t show anything of the sort. For instance, both the Federal Reserve Banks of New York and Atlanta have GDPNow models1 that provide high frequency updates on the health of the U.S. economy with minimal tracking errors. Both now show an annual growth rate of above 2.5% (quarter-over-quarter)2 on a seasonally adjusted basis. That’s around trend for the world’s largest economy and suggests that slack is building at a slower pace than perhaps the market expects. It is quite remarkable when you consider how restrictive the real policy interest rate has been for some time now.

True, there are signs of strain in the labour market. But for now, those are consistent with the slower backdrop you’d expect at this point in the economic cycle, as opposed to anything more nefarious. Monetary policy remains very tight (i.e. interest rates remain high high relative to recent history) and rate cuts should cushion the backdrop against any residual risks that may be building in the system from here. While the ‘soft landing’ scenario has lost some shine of late, it’s still the most likely base case scenario.3

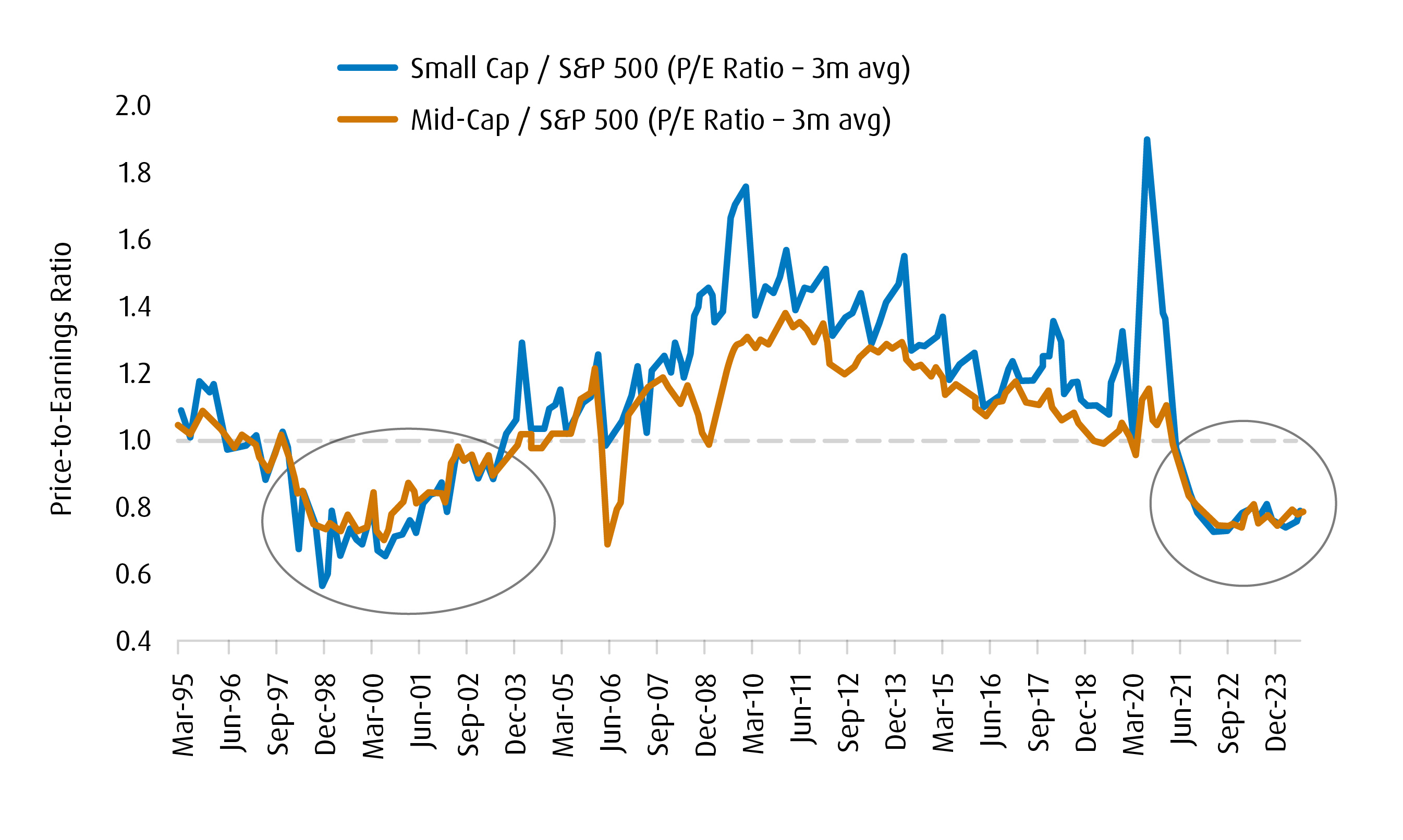

2) Small- and mid-caps are cheap relative to the S&P 500. An easy way to gauge this is by looking at the forward price-to-earnings ratio for small-cap US equities relative to the S&P 500.4 Using Bloomberg’s estimates, we see that the forward P/E ratio for small caps was 0.80x that of the S&P 500. For mid-caps, that ratio is 0.78x.5

The cheaper valuation is only part of the story though. The length of time by which both indices have been undervalued matters here, as well. For instance, both ratios have been below 1.0x for the past three years — the longest such timeframe since the turn of the century. The ratio has been remarkably steady for an unusually long span, and there’s a decent case to be made that it should push higher as investors consider the relatively cheap valuation for small, and mid-caps.

Chart 1 – Small and Mid-Cap Indices: ‘Cheap’ vs. Broader Gauge for Some Time

3) Valuation matters ahead of Fed rate cuts. From prior Fed rate cut cycles, we observe that small/mid-cap valuation relative to the S&P 500 tends to have predictive value over the following six months. For instance, if the P/E ratio for small/mid-caps is above that of the S&P 500, then the former will usually underperform over the course of the next six months (see Table 1). However, given that P/Es for both have been below that of the broader index ahead of the first Fed rate cut, the closest parallel would be with the 2000-2001 cycle – which saw both small/mid caps outperform to a meaningful degree.

Table 1 – Valuation Ahead of First Fed Rate Cut Tends to be Predictive

Cycle Start |

Start P /E Ratio |

Valuation Relative to S&P 500 |

6M Return |

Rule Success or Failure |

|

Small-Cap |

June-95 |

1.06 |

Overvalued |

13.30% |

Success |

Mid-Cap |

June-95 |

1.03 |

Overvalued |

11.33% |

Success |

S&P 500 |

June-95 |

- |

- |

14.45% |

Success |

Small-Cap |

December-00 |

0.72 |

Undervalued |

6.23% |

Success |

Mid-Cap |

December-00 |

0.82 |

Undervalued |

0.97 % |

Success |

S&P 500 |

December-00 |

- |

- |

-6.70% |

Success |

Small-Cap |

August-07 |

1.22 |

Overvalued |

-12.48% |

Partial Success |

Mid-Cap |

August-07 |

1.18 |

Overvalued |

-8.05% |

Partial Success |

S&P 500 |

August-07 |

- |

- |

-8.79% |

Partial Success |

Small-Cap |

June-19 |

1.08 |

Overvalued |

8.00% |

Success |

Mid-Cap |

June-19 |

1.00 |

Fair to slightly Overvalued |

6.97% |

Success |

S&P 500 |

June-19 |

- |

- |

10.92% |

Success |

Past Performance is not indicative of future results. Source: BMO GAM, Bloomberg.

4) Fundamentals matter. As the Fed eases interest rates, small and mid-cap stocks should benefit since the cost of debt servicing is going down. Consider the chart below, which indexes debt growth since the Great Financial Crisis. We see an over six-fold increase in the level of short-term and long-term debt carried by firms that qualify as small-cap. For mid-caps, that figure is closer to four-fold — which is still noticeably larger than the near two-fold increase for the broader market.

That result also compares to what we’ve seen in total debt-to-equity ratios6—as small cap firms have been relying a lot more on debt financing for a while now. Given that a significant portion of these names likely don’t have access to bond markets, it stands to reason that there’s been a lot more reliance on bank lines which are generally floating rate.7 Lower float rates imply lower debt servicing costs for these names. That provides a clearer path to potentially improved income scenarios and ultimately, share price growth.

Chart 2 – Growth in Short- and Long-Term Debt

Based on the dynamics discussed above, investors who see an opportunity in taking an allocation in U.S. mid- and small-cap stocks can consider BMO’s two relevant ETFs, the BMO S&P US Mid Cap Index ETF (Ticker: ZMID) and BMO S&P US Small Cap Index ETF (Ticker: ZSML).

1 GDPNow forecasting models provides the U.S. Federal Reserve a “nowcast” of the official estimate prior to its release by estimating GDP growth using a methodology similar to the one used by the U.S. Bureau of Economic Analysis. GDPNow is not an official forecast. Rather, it is best viewed as a running estimate of real GDP growth based on available economic data for the current measured quarter. Source: Federal Reserve Bank of Atlanta.

2 U.S. Federal Reserve Bank of Atlanta .

3 A soft economic landing is defined by economic growth slowing to a level that brings inflation into central banks’ target range (typically approx. 2%), without triggering a recession. By contrast, a hard landing is when an economy is pushed into contraction by aggressive monetary policy or economic externality.

5 The price-to-earnings ratio (P/E) helps determine the relative cost of a stock, linking market value to profits. P/E ratios are calculated as the ratio of today’s stock price divided by twelve-months’ earnings per share.

5 Bloomberg, as of Sept. 5, 2024. The P/E ratio of a stock is calculated by dividing the current price of the stock by its trailing 12 months’ earnings per share.

6 The debt/equity ratio calculates a company’s financial risk by dividing its total debt by total shareholder equity.

7 A floating interest rate rises or falls with the rest of the market or along with a benchmark interest rate.

Disclaimers

This communication is for information purposes. The information contained herein is not, and should not be construed as, investment, tax or legal advice to any party. Particular investments and/or trading strategies should be evaluated relative to the individual’s investment objectives and professional advice should be obtained with respect to any circumstance. The performance of an Index fund is expected to be lower than the performance of its respective index. Investors cannot invest directly in an index. Comparisons to indices have limitations because indices have volatility and other material characteristics that may differ from a particular mutual fund.

The Index is a product of S&P Dow Jones Indices LLC or its affiliates (“SPDJI”), and has been licensed for use by the Manager. S&P®, S&P 500®, US 500, The 500, iBoxx®, iTraxx® and CDX® are trademarks of S&P Global, Inc. or its affiliates (“S&P”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”), and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by the Manager. The ETF is not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the Index.

BMO Global Asset Management is a brand name under which BMO Asset Management Inc. and BMO Investments Inc. operate.

Commissions, management fees and expenses all may be associated with investments in exchange traded funds. Please read the ETF Facts or prospectus of the BMO ETFs before investing. The indicated rates of return are the historical annual compounded total returns including changes in unit value and reinvestment of all dividends or distributions and do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that would have reduced returns. Exchange traded funds are not guaranteed, their values change frequently and past performance may not be repeated.

For a summary of the risks of an investment in the BMO ETFs, please see the specific risks set out in the BMO ETF’s prospectus. BMO ETFs trade like stocks, fluctuate in market value and may trade at a discount to their net asset value, which may increase the risk of loss. Distributions are not guaranteed and are subject to change and/or elimination.

BMO ETFs are managed by BMO Asset Management Inc., which is an investment fund manager and a portfolio manager, and a separate legal entity from Bank of Montreal.

Any statement that necessarily depends on future events may be a forward-looking statement. Forward-looking statements are not guarantees of performance. They involve risks, uncertainties and assumptions. Although such statements are based on assumptions that are believed to be reasonable, there can be no assurance that actual results will not differ materially from expectations. Investors are cautioned not to rely unduly on any forward-looking statements. In connection with any forward-looking statements, investors should carefully consider the areas of risk described in the most recent prospectus.

The viewpoints expressed by the author represents their assessment of the markets at the time of publication. Those views are subject to change without notice at any time. The information provided herein does not constitute a solicitation of an offer to buy, or an offer to sell securities nor should the information be relied upon as investment advice. Past performance is no guarantee of future results. This communication is intended for informational purposes only.

“BMO (M-bar roundel symbol)” is a registered trademark of Bank of Montreal, used under licence.